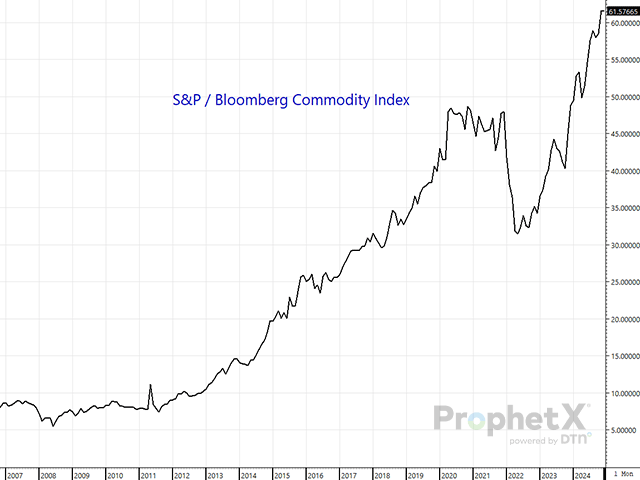

Looking back to the accompanying chart showing the value of the S&P 500 divided by the Bloomberg Commodity Index, you will notice the only real correction that took place in 2022 under circumstances very similar to what we are facing today. Equity markets were overbought, inflation was increasing while being downplayed by the U.S. Federal Reserve and longer-term interest rates were increasing as a result. Sound familiar?

Right out of the gate to start January 2022 trading, profit-taking hit the stock market, and the correction eventually took 27% off the S&P value by early October. By that point, weakening commodity prices inspired optimism that a soft landing for the economy could be accomplished by the Federal Reserve instead of a recession (or worse). It was also increasingly clear that the CPI peaked at 9.1% in June 2022 and was on the decline, allowing the equity bulls to get back to work.

During that period, the Bloomberg Commodity Index increased 40% in value from the start of January to its high in mid-June. A reversal lower in energy markets, when it became clear Russian oil would make it onto world markets, marked the top. By the October low for stocks, the commodity index was still 19% higher on the year.

Will history repeat? No one knows for sure, but the similarities are important enough to seriously consider the possibility. We have already considered how Commodity Index Traders successfully hedged against the first inflationary period (starting in 2019) and how they are currently re-establishing their long hedges. (Read the following blog for more information:

But what about money-managed funds? As we pointed out, they aren’t really concerned about which direction prices are going, as long as they are moving, and that the fund is on the right side of the move. It isn’t hard to figure out which has the better risk/reward profile — being short wheat at $5.50/bushel or long. All it will take is for momentum to shift higher — possibly by actions taken by Commodity Index Traders — to get money managers buying based on the variety of bullish factors out there. Given the fact that they were net short 103,125 contracts, or 515.6 million bushels between Chicago and Kansas wheat futures as of Dec. 10, buying by this group could have a significant impact on prices. Should the fundamentals turn bullish enough to justify, their record net long was a combined 278,270 contracts, or almost 1.4 billion bushels. And that is just an example of the potential for one commodity.

The simple answer is: Yes, it makes perfect sense for a certain amount of money to flow from the stock market into commodity markets. Rest assured, we’ll be on the lookout for triggers and developments.

On a side note, as frustrating as this discussion may be to some, keep in mind it is all part of price discovery. Values may get overdone in both directions, but in the long run, it is the underlying fundamentals that influence decisions made by various participants. If corn celebrated its 50th anniversary at $3.75/bu in the U.S. Midwest this fall (1974 and 2024), with some market participants thinking that was undervalued and wanting to own it as a hedge against inflation, that’s part of price discovery. Or, if money managers weren’t holding a near record long position in live cattle futures based on bullish fundamentals, prices might not be testing record highs. Like it or not, it’s part of the market structure, and the more we understand, the better.

So, as we wind down 2024 and look forward to 2025, put on your optimistic farmer hat and remember: Nothing cures low prices like low prices.

**

Wishing you all the best over the holidays and into the new year! I’m always happy to get feedback along with any suggestions for future blogs.

Mitch Miller can be reached at [email protected]

Follow him on social platform X @mgreymiller

(c) Copyright 2024 DTN, LLC. All rights reserved.